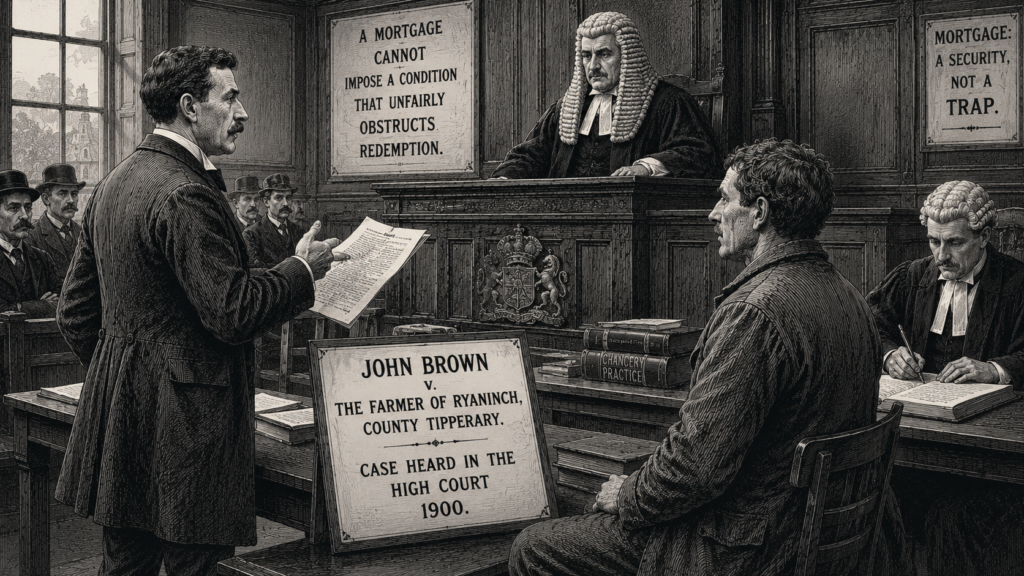

Mortgage Fetter

A mortgage dispute involving County Limerick auctioneer John Browne and Patrick Ryan, a farmer of Ryaninch in County Tipperary, reached the Irish courts in 1900 after Browne sought £62 10s in commission from the sale of Ryan’s property. What appeared to be an ordinary contractual claim raised a larger question about the limits placed upon mortgage lenders. Browne relied upon a separate agreement connected with a £200 loan, but Ryan argued that its terms improperly burdened his right to redeem the mortgaged land and recover complete control once the debt had been repaid.

Ryan had mortgaged lands at Curragh Feakle in County Clare to Browne on 16 June 1898 as security for £200, with interest. Five days later, the parties executed another deed requiring Ryan to sell the property within twelve months through Browne, who was an auctioneer, and to pay him commission of five per cent upon the purchase price. The agreement added that Browne would receive the same commission even if another auctioneer conducted the sale. Both documents formed part of the same financial transaction, although they were contained in separate deeds.

The lands were subsequently sold to a purchaser named Purcell for £1,250 through another auctioneer. Ryan repaid the £200 loan and interest, and Browne reconveyed the property free from the mortgage in November 1898. Browne nevertheless demanded five per cent of the purchase price under the collateral agreement, producing the claim for £62 10s. Ryan resisted payment on the ground that the promise could not be separated from the mortgage. Although the principal debt had been discharged, the commission clause attempted to preserve a further benefit for the lender arising directly from the mortgaged property.

The original trial judge found for Ryan, holding that the agreement constituted an improper clog upon the equity of redemption. A majority in the Queen’s Bench Division later favoured Browne, but the Court of Appeal reversed that decision in November 1900. The appeal judges concluded that a borrower who repaid the mortgage money must regain the land free from an enduring condition created as part of the mortgage transaction. Browne could recover his principal and interest, but he could not enforce an additional advantage that continued to restrict Ryan’s freedom in dealing with the redeemed property.

The ruling reaffirmed the principle commonly expressed in the words “once a mortgage, always a mortgage.” A mortgage could provide lawful security for repayment, but it could not be transformed into a means of obtaining a permanent or oppressive collateral benefit. The case linked a Limerick auctioneer’s commission claim with a doctrine of lasting importance in Irish property law. It also demonstrated how farmers seeking temporary credit might accept complex conditions whose consequences extended beyond repayment. The court’s intervention ensured that redemption restored not merely legal title, but the borrower’s practical freedom to sell and manage the land.

- Browne v Ryan [1901] 2 Irish Reports 653, Court of Appeal in Ireland; argued 6 and 7 November 1900, judgment delivered 23 November 1900.

- The New Irish Jurist, “Browne v Ryan,” report of proceedings on 6, 7 and 23 November 1900, 1 N.I.J.R. 25.

- Law Reform Commission, Consultation Paper on Limitation of Actions, LRC CP 54-2009, Dublin: Law Reform Commission, 2009, paragraph 2.138, note 277.